Tencent: A Valuable Connection

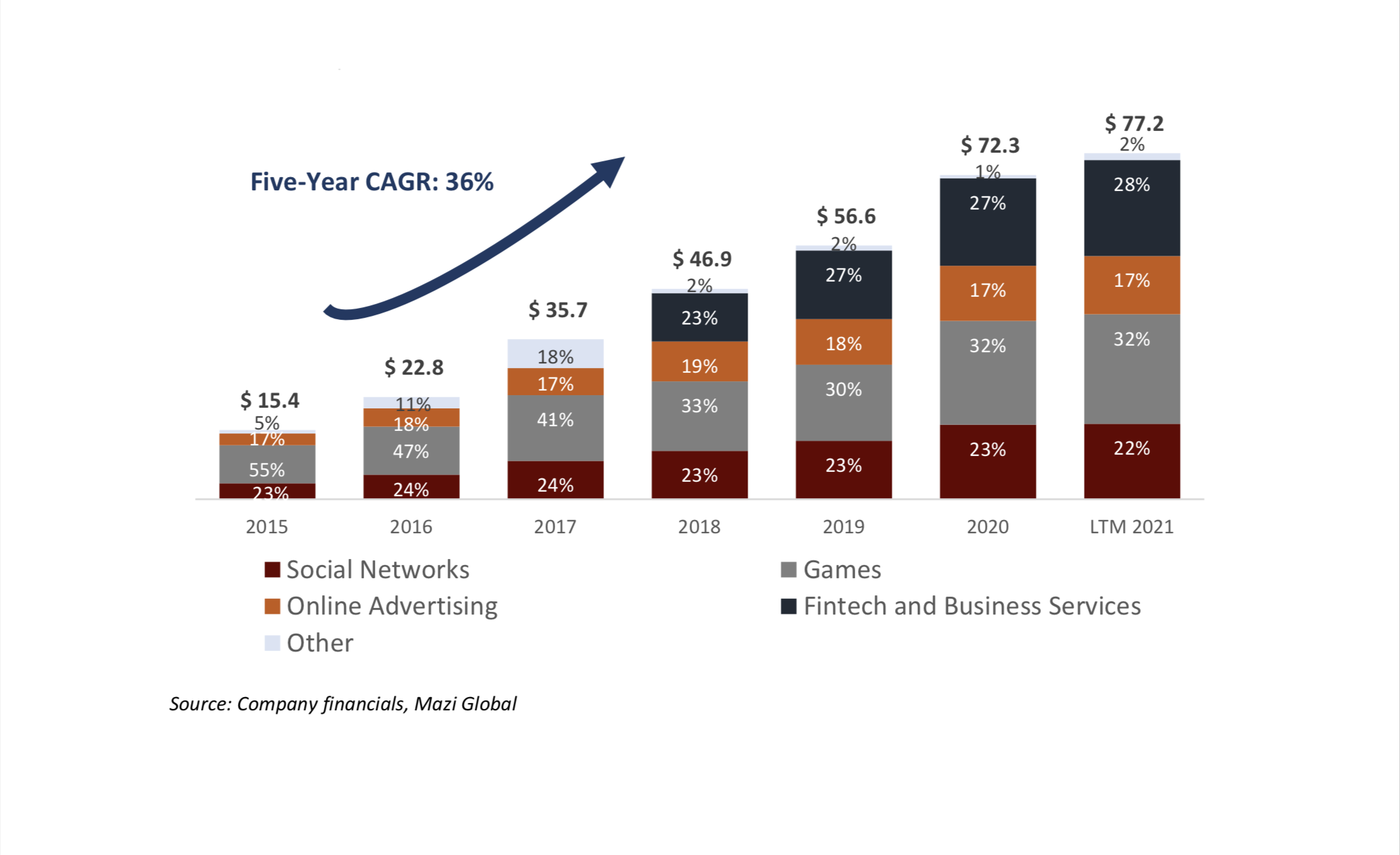

Tencent (Hong Kong-listed with a market-leading capitalisation of US$720 billion) is the dominant Chinese consumer internet conglomerate in gaming, social media, chat, and a significant enabler of online consumer payment. The company also offers cloud computing and business tools to facilitate the mass digital migration of traditional business in China. Additionally, Tencent has a large investee portfolio, a source of considerable untapped long-term investor value, of technology companies, which significantly expands the reach and scope of Tencent’s services. For reference, we present in Table 1 the segmental revenues of the company in US dollar.

From the perspective of an investor, Tencent is an excellent example of a business where the underlying momentum and business growth is not measured in years but is in fact visible for decades to come. These growth characteristics fall neatly within the framework of the Mazi investment philosophy where we seek and own companies that can grow, under their own steam, persistently and profitably over long periods of time. In this article, we discuss the four key tenets that underpin our investment case, highlighting the high-quality, long-term investment opportunity presented by Tencent.

A Leading Network Effect

Tencent’s dominant integrated messaging platforms, WeChat and Weixin, boast a massive userbase of some 1.2 billion monthly active Chinese users. This userbase is Tencent’s crown jewel. For reference, this is a bit less than half of Facebook’s (the leading social network outside China) monthly active user base of 2.9 billion. Within the WeChat-Weixin ecosystem, user-created applications, so-called Mini Programs, enable advanced features that connect hundreds of millions of consumers to small and big business, NGOs and other consumers facilitating e-commerce, gaming, transfer of money and bill payment. In the 2020 reporting period, more than $247 billion of transaction value was generated from Mini Programs alone. WeChat users, using Weixin Pay, make more than one billion daily commercial payments. We expect unabated growth in online commerce and payments services as companies (read: everything from micro enterprises to multinational business) transition to a digital-first existence and marketers adopt an online presence via WeChat. Management continues to enrich the WeChat ecosystem and deepen user engagement.

A Competent Management Team

We have great regard for Tencent’s management. From 2015 to 2020, revenues and profits have grown on a compound annual basis by an impressive 36% and 41%, respectively. This business performance and the sustainability thereof (along with the handy investor returns) are intrinsically a function of managements ongoing ability to lead the business and to consistently execute.

Over time, management has remained flexible and agile, allowing Tencent to gain leading positions in many of its offerings. Tencent successfully embraced the consumer internet market as mobile adoption and internet usage in China accelerated in the early 2000s. Management profitably jumped on the subsequent waves of evolving consumer internet user needs. Today, management’s prescience continues with investment in and aggressive competition in the digitisation of Chinese business, the so-called industrial internet. We view management’s flexibility and ability to spot and monetise key long-term growth opportunities as a key strength of the business and an enabler of multi-year growth.

The Industrial Internet & Cloud Prospects

In cloud, the woolly term used for everything that does not happen on your local computer or handheld device, Amazon is the undisputed leader with a 41% global market share in 2020 in public cloud services, according to Gartner, a technology research group. Amazon earned revenues of $45 billion at an operating margin of 26% in its Amazon Webservices division (which includes its public cloud services) in 2020. Microsoft’s Azure, with a global market share of 20%, has surged to second place with revenues growing 60% in the last year. Its Intelligent Cloud division, which includes legacy server products and Azure, is growing quickly with annualized revenues of $60 billion. As the numbers suggest, the global market opportunity is huge and the overall addressable market continues to expand rapidly, some 41% in the last year alone according to Gartner.

In China, the market opportunity for cloud, a walled internet garden and relatively free from Western competition, is similarly huge and growing. Notwithstanding the boost that the COVID-19 pandemic has given to the digitization of business, global leadership in the industrial internet is an increasing national priority for the Chinese government. Several national champions, most notably Alibaba and Tencent, have been crowded-in to drive the digitization of business and accelerate the internet of things. Tencent’s management has leaped on this opportunity, with its fintech and business services division (under which cloud and industrial internet are reported) growing annual revenues by 32% since 2018 and totaling 28% of revenue in 2020. Practically, the company assists Chinese business to digitize using its cloud infrastructure (migrating on-premises IT hardware to the cloud) and cloud-based office tools, which include WeCom (a business version of WeChat), Tencent Meeting (like Microsoft Teams and Zoom) and Tencent Docs (like Google Docs and Microsoft Office).

The industrial internet is nascent in China. It presents a significant growth opportunity for Tencent, currently the second largest provider in China after Alibaba. Alibaba’s cloud business, for reference, has annual revenues of $8.9 billion and is now cash flow positive, reinforcing the business case. In our analysis, we expect Tencent’s Fintech and Business Services division to sustain a conservative annual compound growth of at least 29% over the next five years, increasing three-and-a-half fold and becoming the largest division by 2025, an estimated 42% of revenue.

The Elevator: A Leading Venture Capital Firm

Tencent has an extensive investee portfolio that does not meaningfully contribute to accounting and cash earnings but represents circa 32% of the company’s total market capitalization. Management has consistently demonstrated a knack for successfully identifying and investing in winning companies. When an investee proves on a stand-alone basis its commercial viability and robustness, it is exposed to Tencent’s 1.2 billion user elevator. Exponential growth usually follows.

By one analysis, Tencent is the largest private technology venture capital ‘firm’ in the world. At the end of June 2021, Tencent held an interest in six companies each with individual market capitalisations exceeding $100 billion and a further sixteen holdings with market capitalisations exceeding $1 billion. As management continues to seek out new investments and capture new growth opportunities, we view this investee portfolio as an ever-growing source of optionality and investor value.

Caveat Emptor

No company is without risks. In Tencent’s life two risks loom large, namely the brutal, incessant competition in China and the endless mounting of Chinese regulatory oversight.

In the case of the former, innovation and ever-changing user needs continually shift existing business models. Moreover, the cross-sectoral expansion of both non-internet and technology companies introduces more players into markets traditionally dominated by either online or offline players. In our view, Tencent will continue to successfully compete given the strength of its adaptability to defend its market leadership positions and seek new growth prospects.

As it pertains to the latter risk, the tech industry has faced a slew of regulation which has resulted in a haemorrhaging of market value. Whilst this has created valuation uncertainty in the medium term as ongoing regulation dampens growth, we view Tencent’s long term investment case as intact.

At present, regulation in China is highly topical. A brief sidebar follows on the matter with a more comprehensive note on regulatory risk available upon request.

In our view, the regulation that seeks to eliminate addictive minor gaming behaviour will have a limited impact upon Tencent as gaming played by minors constitutes 6% of Chinese gaming revenue. Tencent has been proactive (relative to its competitors) in taking measures to limit minor gaming addiction. Moreover, Tencent’s gaming growth vector is now decidedly international. Its gaming portfolio is well positioned to prosper.

Regulation mandating cross-platform interaction will now be possible with the competitors of Tencent gaining access to the company’s gargantuan userbase. Tencent, always pragmatic in its approach to regulation, has halted new registration of WeChat-Weixin users until August, whilst security upgrades are underway. At present, this is not particularly material in the life of Tencent as WeChat-Weixin already has more than 1.2 billion users and is entirely immersed in the daily life of the typical user. Notwithstanding, the potential cannibalisation of payment opportunities on WePay, this regulatory development in fact strengthens Tencent’s position insofar as competitor access to WeChat-Weixin exposes Tencent to whole new data sets and consumer internet interaction. The benefits hereof to Tencent includes increased advertising surfaces, an enhanced understanding of the competitive environment, potential first-mover advantage on consumer trends and a close-up view of possible competitor acquisition opportunities.

Lastly, much of the heat and articles that raise eyebrows on Tencent highlight regulatory scrutiny of its investee portfolio including its live game streaming holdings, e-hailing investee Didi and food delivery company Meituan. The issues range from anticompetitive practice, antitrust to data security concerns. Investees do not contribute towards earnings and therefore any potential impact may reflect through a rerating in the market price of the investee company and consequently Tencent but have no impact on Tencent’s earnings. For regulatory interventions faced by the investees, it remains a matter for the investee to resolve, given Tencent’s hands-off approach to its investee portfolio. Yet, Tencent has not escaped all controversy. Its music streaming subsidiary, Tencent Music, incurred an immaterial financial penalty for incomplete disclosure of past acquisitions and was ordered to give up exclusive music rights. In addition, Tencent’s investees are likely to face delays in listing in markets outside China, due to China’s sensitivity in sharing data (with US regulators being a case in point), the portfolio may face limited expansion as Tencent becomes more selective in new investments and incurs increased compliance costs, and delays in new acquisitions as they comply with antitrust reviews. Our investment case is entirely premised on the continued growth in revenue and earnings in the existing operating business. The investee portfolio offers optionality, and even if some of the investees were to be marked down in valuation, our investment case will still present significant upside from existing operations.

In our view Tencent will continue to focus on product and service innovation, and pragmatically adapt its business to the evolution of the regulatory regime. Regulatory agility and adaptability are straight out of the Tencent playbook.

Always a Margin of Safety

A key component of any investment case, irrespective of the business virtues and underlying quality aspects, is the margin of safety. Investment, at any price, does not happen at Mazi. By our calculations, the market price, on 23 September 2021, offered a 52% discount, that is a margin of safety, to our long-term fair value. The company persistently exhibits the characteristics of a high-quality company, with a long growth trajectory. Whilst we are unable to capture all future growth possibilities in our analysis, we remain confident that Tencent’s ever-widening business moat and capable management team will steer this company through shifting industries, successfully driving the growth of the business over time, and adding much investor value.